What's on this page?

Highlights

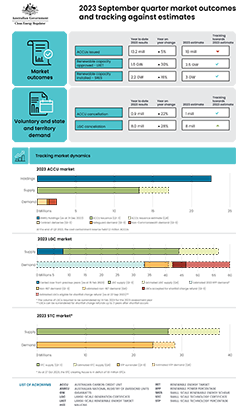

ACCU price stabilises as holdings grow

- The generic spot price for ACCUs traded between $30.50 and $32.00 for much of Q3 2023.

- A quarterly record 7 million ACCUs were issued in Q3 2023 following lower issuances than usual of 6.2 million in the first half of 2023.

- ACCU holdings in the Australian National Registry of Emissions Units (ANREU) increased by 5.9 million in Q3 2023. Safeguard entity holdings increased by 72% and project proponent holdings increased by 24% compared to Q2 2023.

- This suggests some Safeguard entities may be hedging. It is likely Safeguard entities are accumulating ahead of future compliance obligations.

- Project proponents appear to be keeping their options open as the Government considers if the pilot fixed contract exit arrangements will be made permanent. They may also be holding ACCUs for others.

- In Q3 2023, 0.7 million ACCUs were delivered into the cost containment reserve. At the end of Q3 2023, the reserve held a total of 1.2 million ACCUs.

- We have revised our expectations for the 2023 ACCU supply, down from 18 to 17 million. This reflects the increased time to complete human induced regeneration (HIR) gateway audits and lower issuance for landfill gas (LFG) projects.

- Voluntary cancellations continue to grow. 0.3 million ACCUs were voluntarily cancelled in Q3 2023.

- We expect to break the 2022 record of 0.9 million voluntary cancellations in 2023.

Steady pipeline of power stations approvals with growing voluntary LGC demand

- A modest 170 megawatts (MW) reached final investment decision (FID) in Q3 2023, bringing the total for 2023 to 696 MW.

- Approvals of newly completed renewable capacity grew by 608 MW, of which 95% was wind. We are on track to approve around 2.5 gigawatts (GW) in 2023.

- Both LGC supply and demand in 2023 will be at a similar level of about 48 to 50 million, with an effective deficit of about 14.4 million in the market.

- Voluntary cancellations reached 8 million LGCs in Q3 2023. Our estimate has been revised up from 8 to 9.5 million voluntarily cancelled LGCs for 2023.

- 9.5 million represents an additional demand of 29% beyond the Renewable Energy Target (RET).

Record capacity of rooftop solar systems installed

- In Q3 2023, 813 MW of rooftop solar capacity was installed, a Q3 record. We are on track to install over 3 GW of rooftop solar in 2023.

- The average size of rooftop solar systems installed in Q3 2023 was 9.3 kW, another Q3 record.

- An additional 40,000 air source heat pumps (ASHPs) were installed in Q3 2023. Bringing the total for the first three quarters of 2023 to more than 101,000 ASHPs, exceeding the total 87,000 installed in 2022.

- The STC clearing house returned to surplus in Q3 2023. Following the Q3 surrender, the STC clearing house was in a deficit of 1.6 million.

- We expect the clearing house will move back to a surplus before the Q4 surrender in February 2024.

Click on the image below to download a full-sized version.

Data workbook

QCMR data workbook - September Quarter 2023

The Quarterly Carbon Market Report data workbook - September Quarter 2023 contains the data underlying the figures in the report as well as additional data.

Glossary

Our glossary includes definitions/explanations of many terms and acronyms used throughout the QCMR.